Contrate, emplee y pague talento en más de 180 países sin abrir entidades locales

Con gestores de cuenta dedicados, soporte experto real y experiencia práctica en empleo global, Rivermate ofrece a las empresas una forma más práctica de emplear internacionalmente – desde €299.

Recorrido en vivo de 15-20 minutos • Habla con un experto • Sin compromiso

Conoce a Rivermate. Tu globalPotencia en Recursos Humanos

Para personas, por personas

Sin bots, sin tickets perdidos – solo soporte directo y humano. Cada cliente cuenta con un gestor de cuenta dedicado, soporte 24/7 con acceso directo a personal experto a través de múltiples canales de comunicación.

Experiencia práctica

El empleo global es complejo, desde contratos e impuestos hasta legislación laboral y cumplimiento normativo. Con más de 15 años de experiencia, nuestros especialistas internos asumen el trabajo detallado para nuestros clientes, gestionando todo el alcance con rapidez, precisión y una estrecha involucración operativa.

Contratos flexibles adaptados a sus necesidades

Desde subsidios de transporte hasta beneficios de trabajo remoto, adaptamos cada contrato laboral a sus requisitos, no al revés.

Verdaderamente global

Con cobertura en más de 180 países y 38 entidades locales propias, proporcionamos la infraestructura local y el conocimiento del mercado necesarios para un empleo global conforme con mayor cobertura de riesgos.

La rapidez cuando más importa.

Incorporar a los empleados en horas, no en semanas. Mientras otros tardan días en procesar las contrataciones, nosotros le ayudamos a comenzar el mismo día.

Cumplimiento garantizado, riesgos cubiertos

Nuestros especialistas por país garantizan que cada contrato, beneficio y nómina cumpla con las leyes locales. La responsabilidad de cumplimiento es nuestra, nunca suya.

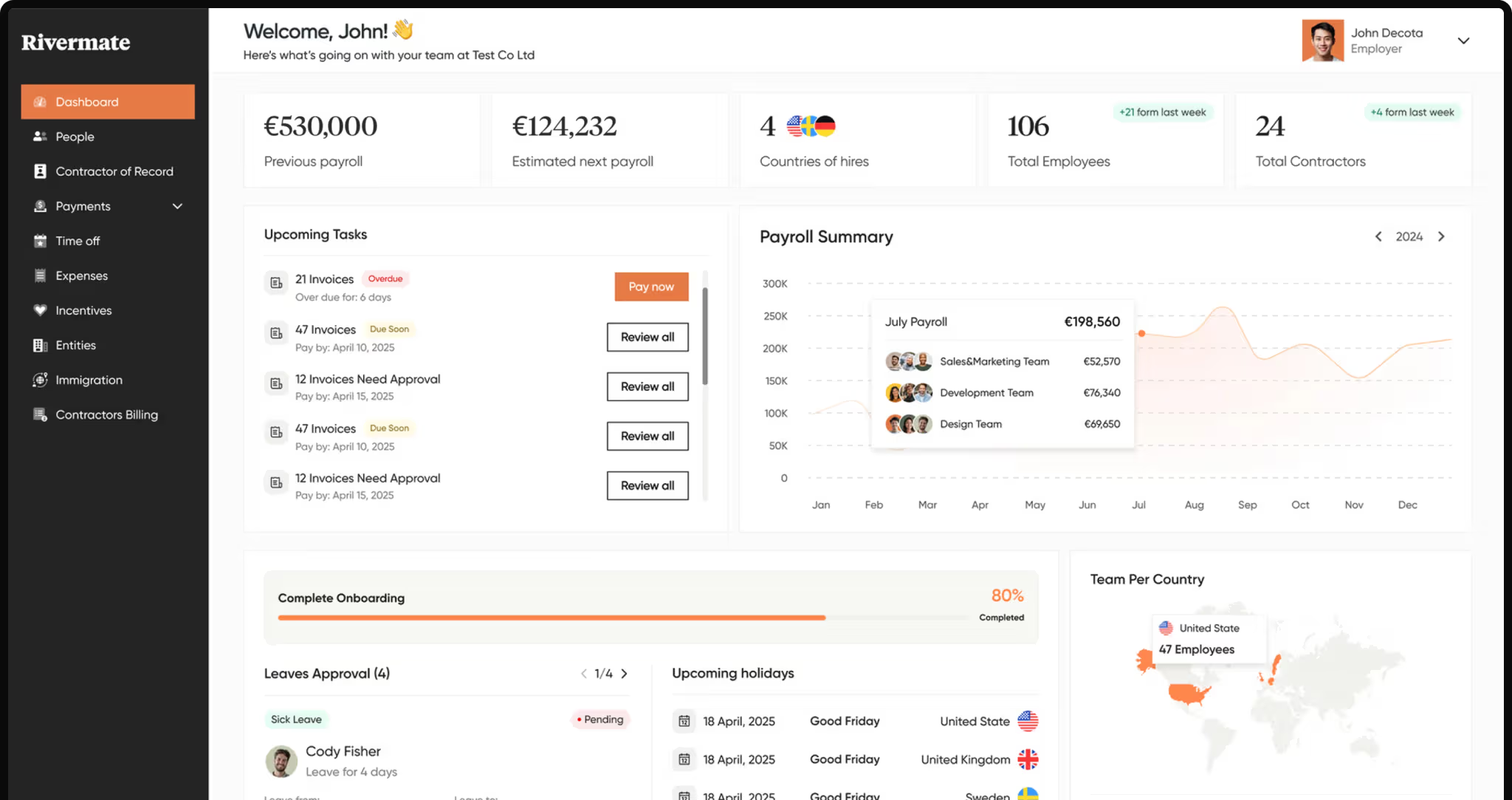

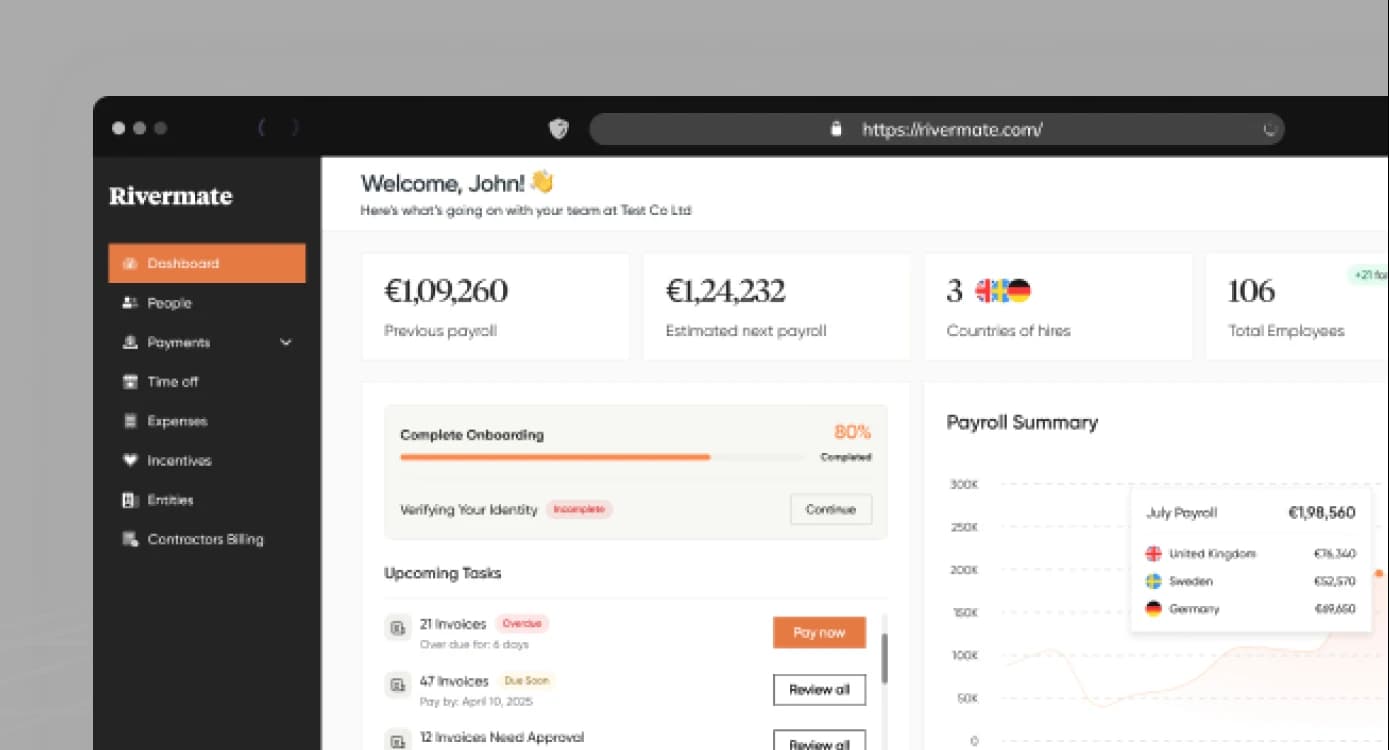

Todo lo que necesitaspara global employment

Contratar empleados a nivel mundial sin entidades locales

Rivermate es su proveedor ideal de Employer of Record (EOR) que ayuda a las empresas a contratar, emplear y pagar talento en más de 180 países sin necesidad de abrir entidades locales. Con soporte personalizado, experiencia interna y una infraestructura global, facilitamos la gestión del empleo internacional.

Entidades propias

38

Empleados contratados

3500+

Nómina anual

€200M+

Empresas ayudadas

1300+

Cómo funciona

Desde el primer clic hasta una nómina global totalmente conforme en cinco pasos sencillos.

Solicitar una demostración

Elija una franja horaria que le convenga. Un especialista de Rivermate le guiará por la plataforma y responderá preguntas de alto nivel.

Propuesta a medida

Desglosamos sus planes de contratación, realizamos una simulación en tiempo real del costo de nómina y enviamos por correo electrónico una cotización única e integral.

Configurar su cuenta

Cree su espacio de trabajo de Rivermate e invite a su equipo. Generamos contratos conformes, recopilamos firmas electrónicas y activamos la nómina.

Escala y relájate: Nos encargamos del resto

Gestionamos la nómina, presentamos impuestos y le mantenemos en cumplimiento en un único panel en tiempo real.

Reconocido por su excelencia por G2

_HighPerformer_HighPerformer.webp&w=256&q=75)

_EasiestAdmin_EaseOfAdmin.webp&w=256&q=75)

_EasiestSetup_EaseOfSetup.webp&w=256&q=75)

_FastestImplementation_GoLiveTime.webp&w=256&q=75)

_BestEstimatedROI_Roi.webp&w=256&q=75)

_EasiestToDoBusinessWith_EaseOfDoingBusinessWith.webp&w=256&q=75)

_BestSupport_Mid-Market_QualityOfSupport.svg)

_EasiestSetup_EaseOfSetup.svg)

_EasiestAdmin_EaseOfAdmin.svg)

Las empresas globales confían en Rivermate para cumplimiento, nómina y soporte — y los evaluadores de G2 están de acuerdo.

Lea reseñas en G2

Por qué las empresas cambian a Rivermate

Soporte personalizado

Experiencia práctica

Verdaderamente global

Soporte personalizado

Gestores de cuenta dedicados, contratos personalizados y soporte 24/7 reactivo

Experiencia práctica

Especialistas internos con más de 15 años de experiencia gestionando contratos, impuestos, legislación laboral y cumplimiento normativo

Verdaderamente global

Más de 180 países cubiertos a través de 38 entidades propias

Otros proveedores de EOR

Soporte personalizado

Chatbots, colas de tickets y soporte más lento y menos personalizado

Experiencia práctica

Soporte estandarizado con poca implicación operativa

Verdaderamente global

Operaciones completamente externalizadas con experiencia local directa limitada